Insurance coverage, premiums, and claim settlements are subject to insurer policy terms, depreciation, and actual loss assessment; declared value does not guarantee full compensation.

Difference Between Declared Value & Insured Value in Packers and Movers

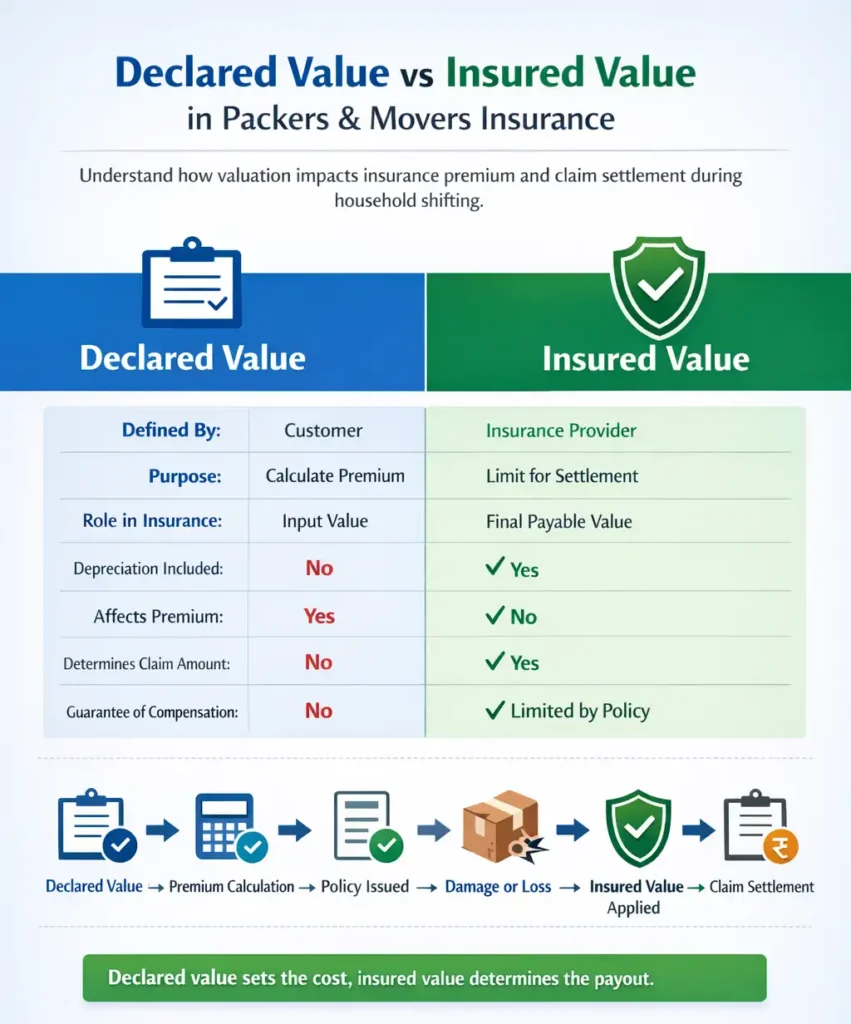

Declared value is the estimated value of household goods declared by the customer to calculate transit insurance premium. Insured value is the maximum amount payable by the insurer during claim settlement after applying depreciation and policy conditions. Compensation is based on insured value, not declared value.

When booking professional packers and movers, most customers focus on packing quality, timelines, and charges—but insurance-related terms often get overlooked. Two of the most misunderstood terms during household shifting are Declared Value and Insured Value. These values directly impact how much protection your goods actually receive during transit and how much compensation you are eligible for in case of damage or loss.

While arranging relocation through a verified service such as Packers And Movers, customers are required to declare the value of their household goods before transportation. This declared figure plays a critical role in insurance premium calculation and claim settlement, yet it is frequently confused with insured value. In reality, declared value does not automatically mean full reimbursement, and insured value is often lower due to depreciation and indemnity principles.

Understanding the difference between declared value and insured value is essential for making informed decisions, avoiding claim disputes, and ensuring realistic expectations during transit insurance claims. As part of smart relocation planning, following expert Moving Tips can help you better understand how insurance works, reduce risks, and make informed choices before your move. This guide explains both concepts in detail, how they are calculated, how they affect insurance premiums, and what really happens during damage or loss claims—using only factual, regulator-aligned insurance principles followed in India.

What Is Declared Value in Household Goods Moving?

Declared Value refers to the total estimated value of household goods declared by the customer before transportation. This value is provided at the booking or survey stage and is used primarily to determine the insurance coverage limit and premium, not the guaranteed compensation amount.

In household shifting, movers do not assess or verify the monetary worth of each item. Instead, customers are responsible for declaring a realistic value that reflects the current depreciated worth of their belongings. This includes furniture, appliances, electronics, kitchen items, and other household goods being transported.

Declared value plays a contractual role in the moving and insurance process:

- It becomes part of the transport and insurance documentation

- It sets the upper boundary for insurance assessment

- It influences how liability is determined if a claim arises

It is important to understand that declared value is an input value, not a payout promise. Insurance follows the principle of indemnity, meaning compensation is limited to actual loss suffered, subject to depreciation and policy conditions. Declaring an inflated amount does not increase claim settlement proportionally, while under-declaring value can significantly reduce claim eligibility.

Key Characteristics of Declared Value

- Declared by the customer, not the mover or insurer

- Used to calculate insurance premium

- Helps define maximum liability exposure

- Incorrect declaration may lead to partial or reduced claim settlement

Common Mistakes Customers Make

- Declaring original purchase price instead of depreciated value

- Under-declaring to reduce insurance premium

- Assuming declared value equals full replacement cost

- Not including high-value items separately

To avoid disputes during claims, declared value should be reasonable, item-inclusive, and aligned with actual usage condition, especially for electronics and appliances.

What Is Insured Value in Transit Insurance?

Insured Value is the maximum amount payable by the insurance provider in case of loss or damage to household goods during transit. Unlike declared value—which is provided by the customer—insured value is finalized by the insurer based on insurance principles, policy terms, and depreciation norms applicable to household items.

In transit insurance for packers and movers, coverage follows the principle of indemnity. This means the insurer compensates only for the actual financial loss suffered, not the replacement cost or emotional value of the items. As a result, insured value is often lower than the declared value, especially for used furniture, appliances, and electronics.

Insured value is determined after considering:

- Declared value submitted at booking stage

- Age and condition of goods

- Applicable depreciation rates

- Type of coverage selected (total loss or partial damage)

To understand what protection actually applies during relocation, it’s important to know what transit insurance covers during house shifting.

Even if a customer declares a high value, the insurer will cap claim settlement at the insured value, ensuring compensation aligns with real-world depreciated worth rather than original purchase price.

Key Characteristics of Insured Value

- Defined by the insurance policy, not the mover

- Represents the maximum claim settlement limit

- Calculated after applying depreciation

- Applicable only if insurance is explicitly opted

Important Clarification

Insured value does not guarantee full reimbursement of declared value. In case of partial damage, insurers assess loss item-wise, and compensation is limited to the insured value of the affected items, subject to policy conditions.

Understanding insured value helps movers set realistic expectations during claim settlement and prevents confusion when compensation is lower than the declared amount.

Declared Value vs Insured Value: Key Differences Explained

Although declared value and insured value are closely connected, they serve very different purposes in the household goods moving and insurance process. Confusing these two values is one of the most common reasons for dissatisfaction during transit insurance claims.

Declared value is the amount stated by the customer before the move, while insured value is the amount the insurer considers as the maximum payable compensation after applying policy conditions and depreciation. Claim settlement is always governed by insured value, not declared value.

Core Differences Between Declared Value and Insured Value

Aspect | Declared Value | Insured Value |

Defined by | Customer | Insurance provider |

Purpose | Insurance premium calculation & liability reference | Claim settlement limit |

Role in claims | Reference value only | Final payable amount |

Includes depreciation | No | Yes |

Guarantee of payout | ❌ No | ✔ Limited to policy terms |

How the Difference Impacts Claims

- Declared value influences how much premium you pay

- Insured value determines how much you can recover

- Over-declaration increases premium without proportionate benefit

- Under-declaration restricts compensation eligibility

During claim settlement, insurers assess the actual loss suffered and compensate the lesser of:

- Actual loss value, or

- Insured value after depreciation

This ensures that compensation reflects financial loss, not replacement or emotional value.

Understanding this distinction helps customers avoid unrealistic expectations and ensures informed decisions while opting for transit insurance during relocation.

How Declared Value Affects Transit Insurance Premium

The declared value of household goods plays a direct role in determining the transit insurance premium during relocation. In household goods insurance, premiums are generally calculated as a percentage of the declared value, making accurate declaration financially important for movers.

Insurance providers use declared value as the base amount for risk assessment. A higher declared value increases the insurer’s exposure, which in turn leads to a higher premium. Conversely, declaring a lower value reduces the premium but also limits claim eligibility in case of damage or loss.

How Insurance Premium Is Linked to Declared Value

- Declared value acts as the premium calculation base

- Premium is charged as a fixed percentage, depending on risk factors

- Higher declared value = higher insurance cost

- Lower declared value = reduced coverage scope

Factors That Influence the Premium

In addition to declared value, insurers also consider:

- Distance of transportation

- Mode of transport (road, rail, containerized movement)

- Nature of goods being moved

- Risk classification of the route

It is important to note that paying a higher premium does not mean full-value compensation. Claim settlement still depends on insured value after depreciation and actual loss assessment.

Risk of Under-Declaring Value

Many customers attempt to reduce moving costs by under-declaring the value of goods. While this lowers the premium, it can result in:

- Partial claim settlements

- Compensation far below actual loss

- Disputes during claim processing

For a balanced approach, declared value should reflect the realistic depreciated worth of household items rather than original purchase price or arbitrary estimates.

What Happens During Damage or Loss: Claim Settlement Process

When household goods suffer damage or loss during transit, claim settlement is carried out strictly according to insurance policy terms and the principle of indemnity. This means the insurer compensates only for the actual financial loss incurred, subject to the insured value and applicable depreciation.

The claim process does not rely on declared value alone. Instead, insurers evaluate the loss against the insured value of the affected items, ensuring that compensation does not exceed the policy’s maximum payable limit.

Step-by-Step Claim Settlement Flow

- Intimation of Loss

The customer must inform the insurer within the specified time after delivery. - Submission of Documents

Commonly required documents include:- Insurance policy copy

- Declared value statement

- Packing list

- Damage photographs

- Claim form

- Assessment of Damage

The insurer evaluates:- Nature of damage (partial or total)

- Age and condition of the item

- Depreciation applicable

- Insured value limit

- Claim Approval & Settlement

Compensation is calculated as the lower of actual loss or insured value, after depreciation and policy deductions.

Partial Damage vs Total Loss

- Partial Damage:

Compensation is calculated item-wise, not on the total declared value. - Total Loss:

Settlement is capped at the insured value, even if declared value is higher.

Impact of Incorrect Declared Value

- Under-declared value can lead to proportionately reduced claims

- Over-declared value does not increase payout beyond insured limits

- Mismatch between declared items and damaged items may delay claims

Understanding this process helps movers set realistic expectations and avoid disputes during insurance settlement.

Many claim disputes arise because customers are unaware of exclusions, depreciation rules, and policy conditions explained in why insurance claims get rejected during house shifting.

How to Choose the Right Declared Value for Your Move

Choosing the right declared value is one of the most important steps when opting for transit insurance during household shifting. An accurate declared value ensures that insurance coverage remains cost-effective, while still offering meaningful protection in case of damage or loss.

Declared value should represent the current depreciated value of your household goods—not the original purchase price or replacement cost. Insurance compensation is always aligned with actual financial loss, so realistic valuation helps avoid both overpayment of premium and claim shortfalls.

Practical Guidelines to Determine Declared Value

- Assess goods room-wise

Estimate the value of items in each room instead of using a lump-sum guess. - Apply depreciation logically

Older furniture, appliances, and electronics should be valued lower based on usage and age. - Identify high-value items separately

Electronics, appliances, and fragile items should be distinctly accounted for. - Avoid intentional under-declaration

Lower premiums may look attractive but can severely limit compensation. - Use professional pre-move surveys when available

Surveys help in documenting items accurately, reducing claim disputes.

Common Valuation Errors to Avoid

- Declaring original invoice value

- Ignoring depreciation for used items

- Excluding fragile or high-risk goods

- Declaring round figures without item-level logic

For first-time movers, valuation errors are common due to lack of familiarity with insurance norms. Taking a balanced and realistic approach to declared value ensures smoother claim processing and better alignment between declared and insured values.

Common Myths About Declared Value and Insurance Coverage

Misunderstandings around declared value and insured value often lead to unrealistic expectations during transit insurance claims. Clarifying these myths helps movers make informed decisions and avoid disputes at the settlement stage.

Myth 1: Declared Value Equals Full Compensation

Reality: Declared value is not a payout guarantee. Compensation is limited to the insured value after depreciation and actual loss assessment. Even a high declared value does not ensure full reimbursement.

Myth 2: Movers Automatically Insure Goods

Reality: Insurance is not automatic. Transit insurance must be explicitly opted for, and coverage applies only when a valid policy is issued.

Myth 3: Insurance Covers Every Type of Damage

Reality: Policies generally exclude wear and tear, mechanical failure, and pre-existing damage. Only transit-related, accidental damage is considered, subject to policy terms.

Myth 4: Under-Declaring Value Has No Consequences

Reality: Under-declaration can lead to proportionate reduction in claim settlement. If the declared value is significantly lower than actual loss, compensation may be inadequate.

Myth 5: Emotional or Replacement Value Is Considered

Reality: Insurance follows the indemnity principle. Claims are settled based on financial loss, not sentimental or replacement value.

Understanding these myths reinforces why it is critical to declare value realistically, opt for insurance consciously, and read policy terms carefully before relocation.

Before finalising your move, reviewing a professional packers and movers hiring checklist can help avoid valuation mistakes and insurance-related disputes.

FAQs: Declared Value vs Insured Value

Declared value is the estimated value of household goods provided by the customer before the move, mainly used to calculate the insurance premium. Insured value is the maximum amount the insurer may pay during claim settlement after applying depreciation and policy conditions. Compensation is always based on insured value, not declared value.

Yes, declared value is required to calculate the insurance premium and define the coverage scope. Without declaring the value of goods, transit insurance cannot be issued for household shifting.

No. A higher declared value increases the insurance premium but does not guarantee higher compensation. Claim settlement is limited to the insured value and actual loss suffered, after depreciation.

Insured value is calculated by applying depreciation to the declared value of goods, considering their age, condition, and usage. This value represents the maximum payable amount during claims.

Under-declaring value may reduce insurance premium, but it can lead to proportionately lower compensation or partial claim settlement if damage occurs during transit.

No. Transit insurance for household goods follows the indemnity principle, which means compensation is based on actual financial loss, not replacement or emotional value.

Compare verified packers and movers, declare the right value for your household goods, and opt for transit insurance that truly protects your move.

If you are planning a household move in Trichy, working with verified packers and movers in Trichy ensures transparent valuation, proper documentation, and insurance support.